Data Vizualiation

This project uses data of different economic indicators that are available on the Federal Reserve Bank of St. This includes, The Homeownership rate in the United States, Median Sales Price of Houses Sold for the United State, Personal Saving Rate, Unemployment Rate, and Federal Funds Effective Rate. Click here to view the data set.

Figure 1:

Figure 1 illustrates the count of car accidents by day between 2016 to 2021. We see an increasing trend of car accidents throughout time and especially after October 2020. When we zoom in closer, we see a trend of weekly seasonality, where the highest peak of incidents is on Fridays and the lowest number of incidents is on Sundays. This trend can be explained by the fact that people spent longer time traveling to weekend getaways, drunk driving, or simply a higher volume of cars out on the roads to enjoy the weekend. From the data viz alone the trend seems additive.

Figure 2:

Figure 2, above, displays interest rates over time. We can see that interest rates in 1980 were higher than 15 percent and have shown a decreasing trend with signs of seasonality.

Figure 3:

Figure 3 above shows the relationship between homeownership, interest, and unemployment rates between 1980 and 2022. When the unemployment rate is high, the homeownership rate declines; this is particularly visible in the late 2000 and early 2010s. The relationship between interest rates and the homeownership rate is less pronounced in Figure 3.

Figure 4:

Figure 4 above explores the relationship between homeownership and average personal savings rates. While a high average personal savings rate is an excellent economic indicator in the long run, it also tends to increase during economic slowdowns or times of uncertainty. For example, as shown in Figure 4, in 2020, during the Covid pandemic, the average personal saving rate was over 26 percent. As seen in Figure 4 above, we see that the average personal savings rate is inversely related to the homeownership rate.

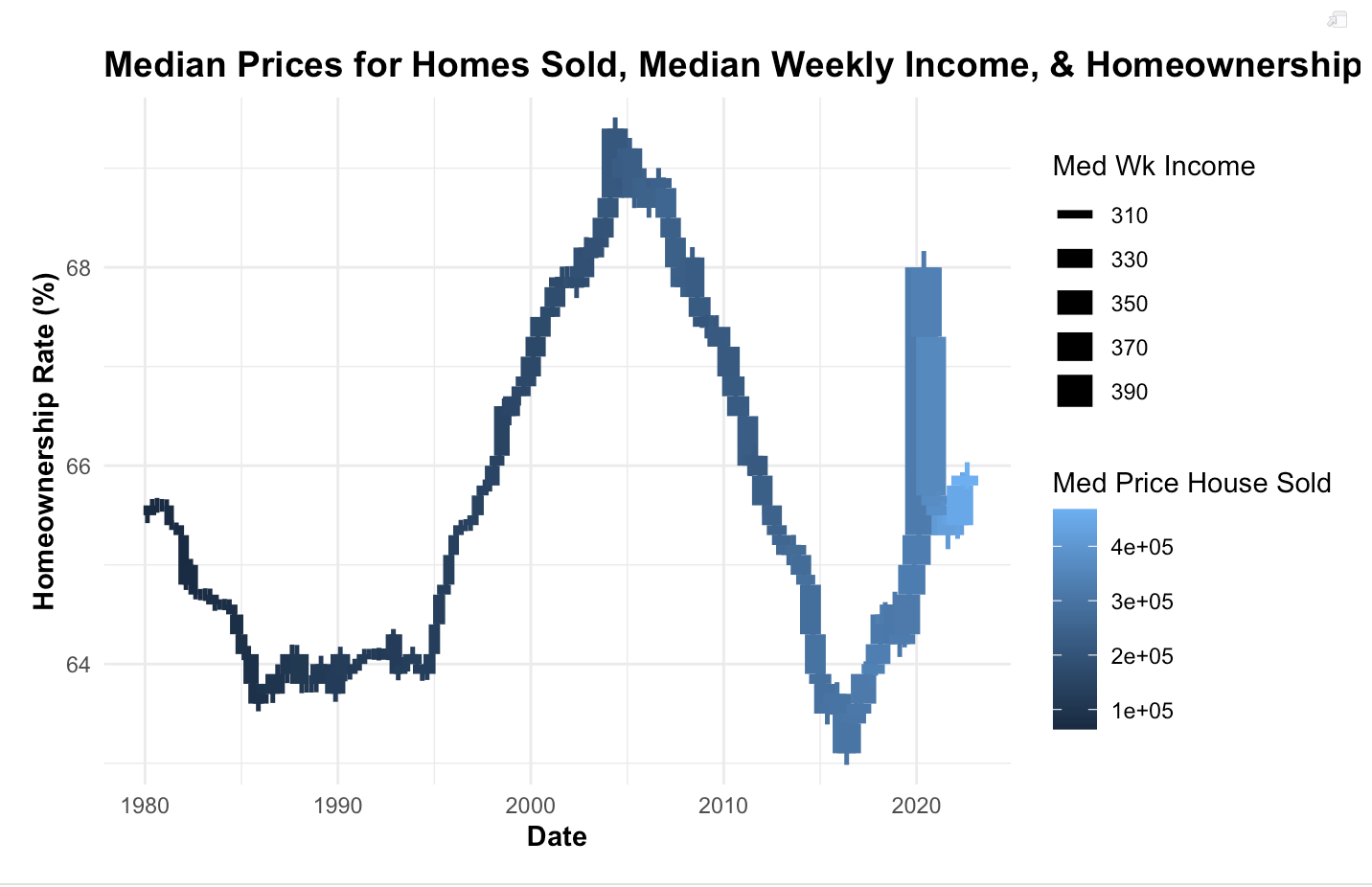

Figure 5:

Figure 5 above explores the relationship between the median weekly household income, the median home sale price, and the homeownership rates. The relationship between the three variables is not as pronounced in the figure above; However, we can see that when the median weekly household income is low, homeownership is also low before the mid-2000s.